Adopting a Lifestyle Compatible with Classified Work

One of the more painful moments for a security clearance lawyer is watching Department Counsel, sworn to strip your client’s clearance, cross-examine them in a Guideline F, Financial Considerations proceeding. The careers of many a Federal employee, contractor, and service member depend upon an active security clearance. Yet, many do not understand: one cannot live how uncleared people do. This is never more evident than when Department Counsel bores into the lifestyle decisions underlying debt sufficient to trigger a security concern. You may think your decisions were typical, even appropriate, given your family members’ and friends’ experiences. But the “typical” standards may not be sufficient to keep a clearance.

Many government positions require a security clearance. Eligibility for access to classified information is a privilege, as is working with material shielded from the general public. Numerous concerns dictate eligibility, and personal credit history is heavily weighted. If you want to live like many other Americans, avoid a clearance. Most Americans cannot be given access; they lack the discipline needed to avoid the financial straits that would make them prime targets for foreign intelligence operatives.

A low credit score can jeopardize your chances of obtaining or maintaining a security clearance. But do not despair if you just had a run of back luck. SEAD-4, the applicable regulation, allows for mitigation of some financial failures. But first, you must recognize in your head and heart: you failed.

How Does Credit Affect Your Security Clearance?

Credit history serves as a primary indicator of your overall reliability, trustworthiness, credibility, and good judgment. Adjudicators evaluate your background to determine if your actions pose an unacceptable risk to national security. This area of inquiry is also relatively ‘easy’ to pursue, as much of the data is available in digital form and readily available through Continuous Evaluation (CE) collection. It is not hard to do, unlike foreign contact assessment. The Federal government will be rid of debtors far sooner than it will be rid of all spies. Consider the following to avoid becoming one of them:

The Vulnerability Risk:

Financial distress can signal poor self-control or lack of judgment. Individuals facing overwhelming debt may become targets for foreign intelligence services, corporate espionage, or malicious actors seeking to exploit financial vulnerabilities. The burden is on you to prove otherwise. Be mindful of how you might prove you do not lack self-control, and gather that evidence.

Compromising Behavior:

Severe financial pressure could make a person more susceptible to accepting bribes or disclosing sensitive information in exchange for financial relief. How do you prove you are not prone to such manipulation? The burden is on you.

National Security Implications:

The federal government scrutinizes credit histories across all clearing bodies, with particular focus on military personnel and Department of Defense (DoD) contractors handling highly sensitive technologies. So, pull your credit history every two years. Ensure it has nothing on it that does not belong to you. And if a debt does belong to you, work to remove it without accepting a discharge of the debt or a mark-down of the same.

What Investigators Look for in Your Financial History

Background investigators do not just check your credit score; they perform an in-depth review of your entire credit report to look for:

- Patterns of Irresponsibility: Investigators look for systemic financial issues, including a history of late payments, account defaults, charged-off accounts, or items sent to collection agencies.

- Red Flags: Demonstrating an inability or systemic unwillingness to satisfy outstanding debts serves as a significant red flag. This behavior can lead directly to a clearance denial or revocation.

- Favorable Actions: Creating an active, documented plan to address your debt—such as working through reputable credit counseling services—is viewed very favorably during the adjudication process. But do not turn your debt recovery over to the third-party counseling service. Adjudicators want to see evidence you are directing the effort.

See Your Personal Finances Through Security’s Eyes

The inability to live within one’s paycheck is a ticket back to an unclassified career. And while many take part in the gig economy, the Security standard is: “no side-hustles.” Gig work can lead to numerous security concerns. So, if you have streams of income other than your classified job, ensure they are all appropriately documented and approved by Security and the Designated Ethics Officer (DEO). The Federal government provides its employees, contractors, and service members an income which they are expected to budget appropriately. It is all Security thinks one needs to live a happy and prosperous lifestyle.

Guideline F (Financial Considerations) remains the most common security concern, prompting the lion’s share of security clearance denials and revocations. In many instances, unresolved financial distress is what tips the scales to an unfavorable clearance determination.

Failing to disclose financial issues on your Standard Form 86 (SF-86) is often treated more severely than the debt itself. Hiding or withholding information indicates a lack of candor: an immediate red flag that can derail your application.

Not paying your taxes is behavior puzzling to Security: why would they grant you a clearance to work for the very government you have cheated out of lawful taxation approved by your Member of Congress? Even failing to file when the U.S. Government owes you money is a security concern. Who wants to work with a fellow employee who cannot follow directions? That is the Security logic: think like Security, be approved by Security.

Having bad credit is not an automatic, permanent disqualifier for a security clearance. It is, however, heavily weighed during your background evaluation. Investigators also note mitigating factors, like responsible efforts to dig your way out of debt.

Time was, you could file for bankruptcy and still gain a clearance within three years. Very difficult to do that now. Filing for bankruptcy is a major financial event that triggers an automatic review of your clearance eligibility, but it is not an absolute disqualifier. The root cause of the bankruptcy determines how adjudicators perceive it.

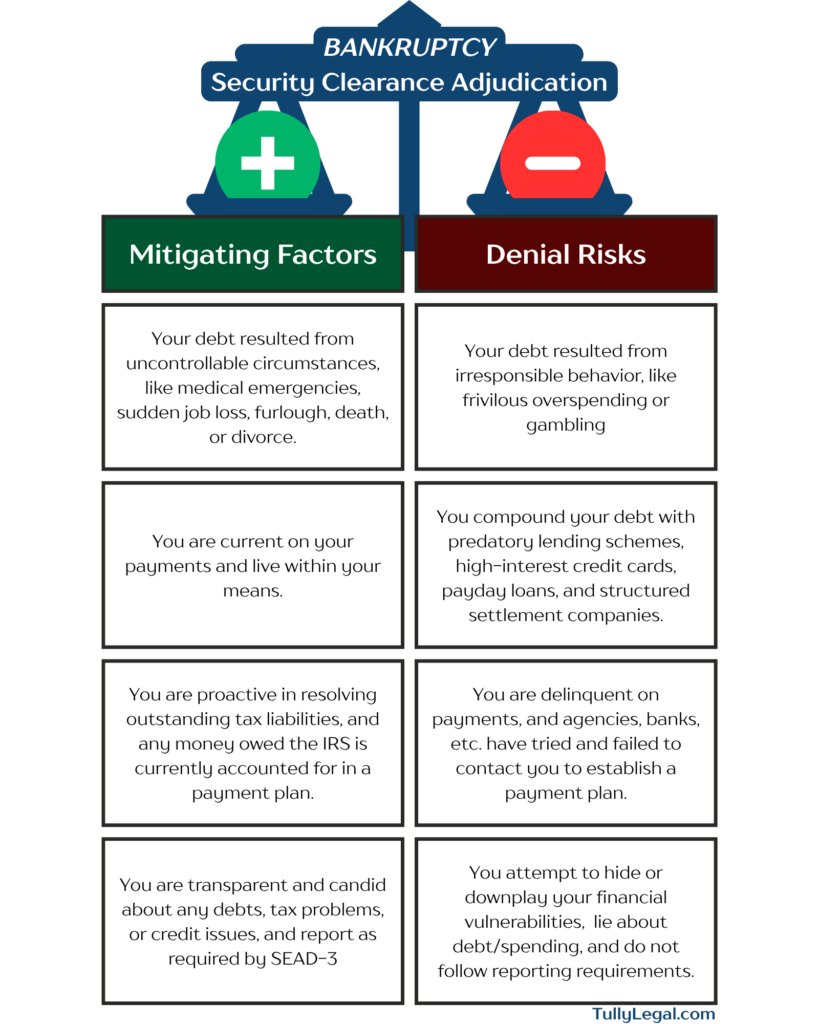

Bankruptcy’s Impact on Your Security Clearance

The reason for bankruptcy is itself highly relevant to Security. Bankruptcy resulting from Uncontrollable Circumstances (e.g., medical emergencies, sudden job loss, divorce) may be viewed more leniently as an isolated, unpreventable event. When debts are legally structured or discharged, a favorable Security determination becomes more likely.

By contrast, bankruptcy resulting from Irresponsible Behavior (e.g., frivolous overspending, reckless gambling) is more likely to be perceived as a sign of poor judgment and poor self-control. Such circumstances come with a high risk of security clearance denial or revocation.

If you file for bankruptcy, you must provide clear documentation showing a stable financial plan moving forward. There is no specific dollar threshold that automatically disqualifies you from holding a security clearance. Adjudicators look at the ratio of your debt relative to your income, as well as how orderly you are in managing your obligations.

Avoiding and Resolving Financial Issues

Debt Management: Even a high debt-to-income ratio can be mitigated if you remain current on your payments and live within your means.

Young Recruits and the Military: Young service members often fall prey to predatory lending traps, high-interest credit cards, or payday loans due to a lack of early financial literacy. This early indebtedness frequently blocks them from getting clearances later in their military careers. Learning to spot and steer clear of these predatory cycles is essential for long-term career growth.

File and Pay Your Taxes: As we have detailed above, one’s tax history is treated with absolute severity by federal adjudicators. A history of failing to file annual federal, state, or local tax returns, or failing to pay tax liabilities, is a major Guideline F violation.

Proactive Resolution: You must resolve outstanding tax liabilities before applying for a clearance. If you owe money to the IRS, establish an official installment agreement and remain strictly compliant with it.

Total Transparency: Always be completely honest about past tax problems on your SF-86. Never try to hide, obscure, or downplay past tax issues; an intentional omission will severely damage your credibility.

Whole-Person Analysis

The evaluation rests entirely on the context of the whole-person concept. So, a low credit score or significant debt burden will not automatically bar one from public trust or classified roles, provided you manage the situation correctly. You cannot correctly manage a situation outside your awareness.

For security clearance purposes, managing the situation requires that you:

Be Proactive: Tackle outstanding balances, resolve collections, and set up payment plans before you submit your paperwork.

Be Transparent: Disclose all delinquent financial items honestly during your application and background interview sessions.

If you have concerns about how your past finances could impact your eligibility, a security clearance attorney can provide confidential guidance. Unlike asking your agency or FSO, bringing concerns to counsel does not risk your national security eligibility. An adjudication-tested attorney will unpack the complexities of the clearance process and, more importantly, build a structural actionable plan to resolve potential red flags.

Dan Meyer, Esq. is a Partner at Tully Rinckey PLLC’s Washington, D.C. office and has dedicated more than 25 years of service to the field of Federal Employment and National Security law as both a practicing attorney and federal investigator and senior executive. He is a lead in advocating for service members, Federal civilian employees, and contractors as they fight to retain their credentialing, suitability and security clearances.

Tully Rinckey attorneys understand that issues involving security clearances and financial issues can be challenging, and they will handle your matter with the attention and tact it deserves. If you have additional questions, our team of dedicated security clearance attorneys is available to assist you today. Please call 8885294543 to schedule a confidential consultation, or schedule your consultation online.